From Statement of Values to Smart Asset Registry: Preparing FEMA PA Applicants for Cost-Estimate-Driven Disaster Funding

The insurance Statement of Values is no longer enough for disaster finance. This Govstar resource explains how governments can convert SOV data into a FEMA-ready Smart Asset Registry that supports upfront funding, cost estimates, parametric triggers, insurance recovery, and audit-ready closeout. Topics include COPE data, FEMA PA eligibility, legal responsibility, pre-disaster condition, replacement cost, hazard exposure, mitigation fields, damage-to-cost formulas, basis risk, settlement protocols, DOB controls, dashboards, and a phased roadmap from SOV cleanup to parametric-enabled recovery planning.

From Statement of Values to Smart Asset Registry: Preparing FEMA PA Applicants for Cost-Estimate-Driven Disaster Funding

How governments can transform insurance Statements of Values into Smart Asset Registries for FEMA PA cost estimates, upfront funding, disaster recovery, and parametric triggers.

Important Status Note: HR4669 and the FEMA Review Council recommendations referenced throughout this article should be treated as proposed reform concepts unless enacted, adopted, funded, and implemented through binding law, regulation, or FEMA policy. Current FEMA PA eligibility still turns on existing Stafford Act, 44 CFR Part 206, and FEMA policy requirements. Under current 44 CFR § 206.223, eligible PA work must be required as the result of the disaster, located in the designated area, and be the legal responsibility of an eligible applicant.

The Big Shift: Why the Insurance SOV Is No Longer Enough

For decades, public entities have maintained a Statement of Values, or SOV, primarily as an insurance underwriting tool. The SOV tells insurers what assets exist, where they are located, and what they are worth. It supports property insurance placement, catastrophe modeling, sublimits, deductibles, total insurable value, and insurance-to-value analysis.

But the future FEMA Public Assistance environment may require something more powerful.

The SOV has served as the "census" of a policyholder's assets — capturing location ID, physical address, latitude and longitude, building value, business personal property, business interruption/extra expense, inventory, ISO construction class, year built, square footage, number of stories, occupancy, sprinkler status, public protection class, alarms, roof data, opening protection, basement/pit information, and other primary and secondary COPE fields.

That is a strong insurance start. But it is not enough for the next generation of disaster finance.

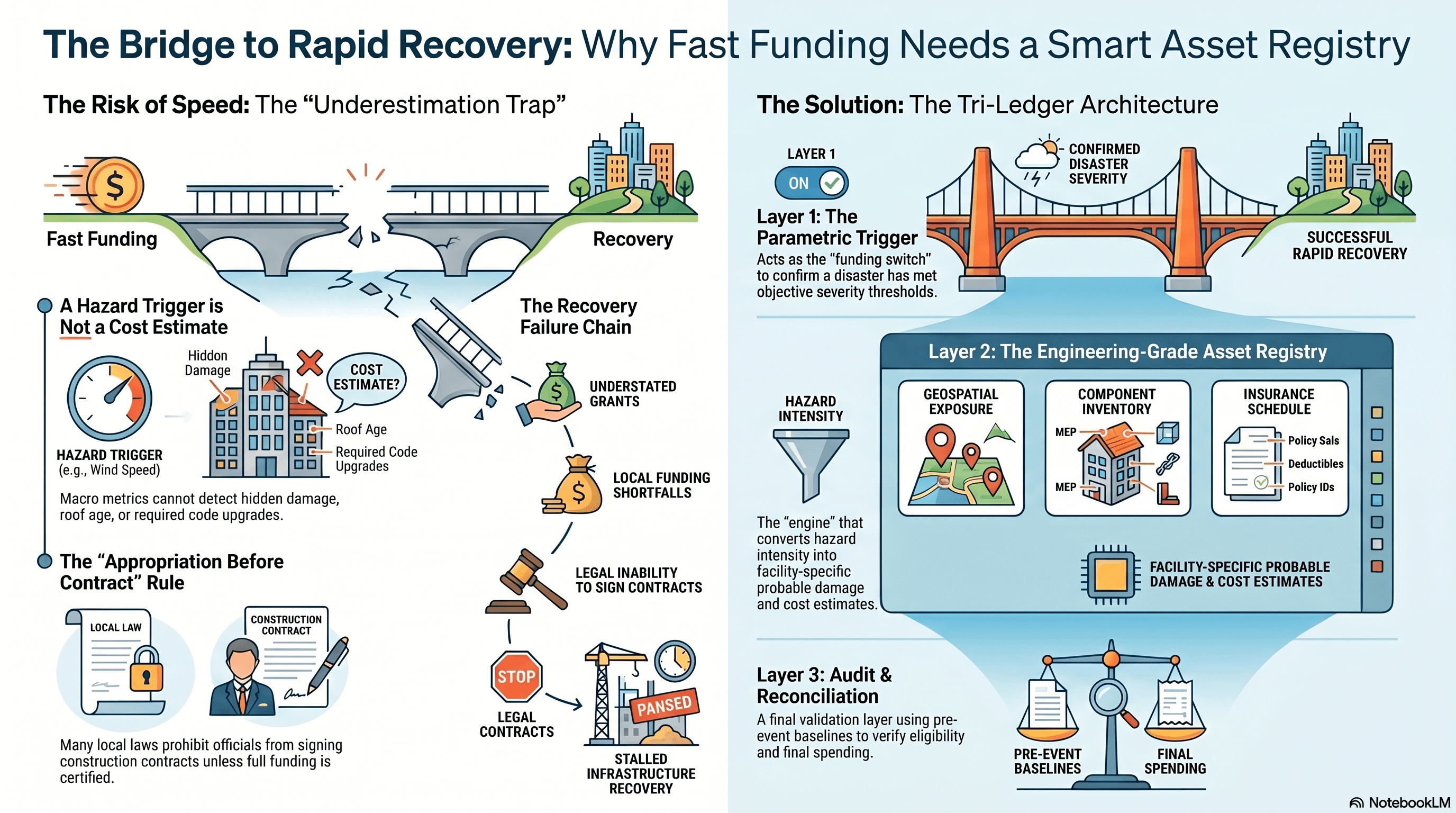

That difference matters because HR4669's proposed Public Assistance reforms would move the center of gravity toward professional cost estimates, faster review, upfront grant availability, mitigation-informed repair, and resilience incentives. The proposed §409 model is not merely an administrative shortcut — it is a new way to think about the disaster recovery data stack. If grant amounts are based on cost estimates, the quality of the applicant's pre-disaster asset data becomes central.

The best-positioned applicants will not be those who begin collecting facility data after landfall, fire, flood, or earthquake. The best-positioned applicants will already have an asset registry capable of generating defensible initial cost estimates.

What a Traditional Statement of Values Does Well

The traditional SOV is still essential. It should not be discarded — it should be upgraded. The SOV typically provides five core functions:

1. Location Identification. Each site should have a unique location number, physical address, city, state, ZIP code, county, and latitude/longitude. Accurate geocoding is critical for catastrophe modeling, especially for wind, flood, earthquake, and high-hazard areas.

2. Total Insurable Values. These include building value, business personal property, business interruption/extra expense, inventory, and other valued exposures. These values support insurance-to-value analysis, capacity placement, deductibles, sublimits, and catastrophe modeling.

3. Primary COPE Data. COPE stands for Construction, Occupancy, Protection, and Exposure — the underwriting basics: construction class, occupancy description, year built, square footage, number of stories, and basic fire protection.

4. Protection and Engineering Information. For public-sector portfolios, this may include sprinkler type, water supply, public protection class, monitored alarms, generator protection, backup power, and essential service continuity features.

5. Secondary COPE Fields. Increasingly important for catastrophe modeling, these include roof geometry and material, year of major roof/HVAC/electrical/plumbing updates, opening protection, basement/pit details, and flood vulnerability indicators. Absent secondary COPE data, catastrophe models may default to conservative or worst-case assumptions.

For insurance underwriting, these data points are useful. For FEMA Public Assistance, they are only the beginning.

A FEMA-ready Smart Asset Registry must extend the SOV in at least six ways:

Document pre-disaster condition

Support facility eligibility and legal responsibility

Classify assets by FEMA PA category and facility type

Support rapid damage-to-cost conversion

Identify codes, standards, mitigation, and resilience gaps

Connect physical asset data to insurance, parametric triggers, and recovery funding sources

Under current PA regulations (44 CFR § 206.223), the work must be required by the disaster, located in the designated area, and be the legal responsibility of an eligible applicant. A Smart Asset Registry should therefore help prove not just value, but eligibility, location, ownership/legal responsibility, pre-disaster condition, and disaster-caused scope.

What Makes an Asset Registry "Smart"?

A Smart Asset Registry is not simply a bigger spreadsheet. It is a disaster finance database. It combines insurance underwriting data, engineering data, FEMA eligibility data, cost-estimating data, hazard exposure data, mitigation data, and parametric-trigger data into one structured asset record.

Consider the difference:

Traditional SOV Entry: Fire Station 12 — $8.5 million building value — 21,000 square feet — masonry construction.

Smart Asset Registry Entry: Fire Station 12 is a legally owned public safety facility, Category E building and equipment asset, located at verified latitude/longitude coordinates, with ISO Class 4 masonry non-combustible construction, a replacement cost new of $8.5 million, roof replaced in 2021, emergency generator elevated above base flood elevation, electrical switchgear located in the basement, flood depth vulnerability at 18 inches above first-floor elevation, pre-disaster condition photos updated annually, insured under property policy schedule location 12, and mapped to a wind parametric grid cell and flood gauge trigger zone.

The second record is far more useful after a disaster. It can support:

Insurance claim validation

FEMA damage inventory

Preliminary damage assessment

Cost estimating

Mitigation scoping

Parametric payout calculations

Capital planning

Bond disclosure

Grant closeout

Audit defense

This additional "DNA" is the difference between a passive insurance list and an active recovery tool.

The HR4669 Connection: Why Initial Cost Estimates Change the Data Requirement

The proposed HR4669 §409 model is the reason this matters now.

Under the proposed language, grant amounts would be determined based on the estimated cost to repair, restore, reconstruct, or replace a damaged public or private nonprofit facility to applicable building codes. The estimate must be developed by an appropriately licensed professional and must include:

Mitigation measures

Labor costs

Management costs

Materials

Other repair/restoration/reconstruction/replacement costs

The cost of developing the estimate

The same bill excerpt proposes a 90-day review period after submission of the estimate, a 30-day deadline for making funds available after approval, a one-time adjustment within two years for market changes, and finality protections absent criminal fraud.

That structure radically increases the value of pre-disaster asset data.

If the applicant has poor data, the estimate process becomes slow and reactive. Engineers must locate drawings, confirm dimensions, investigate construction type, determine roof age, identify MEP location, obtain photos, determine code triggers, and reconstruct pre-disaster condition — all after the event.

If the applicant has a Smart Asset Registry, much of that work is already structured. The registry becomes the pre-disaster baseline for:

FEMA already recognizes cost estimating as part of PA administration through its Cost Estimating Format (CEF), described as a uniform methodology for determining costs of eligible permanent work for large construction projects. The proposed HR4669 model would make this even more critical because the cost estimate itself becomes the gateway to upfront funding.

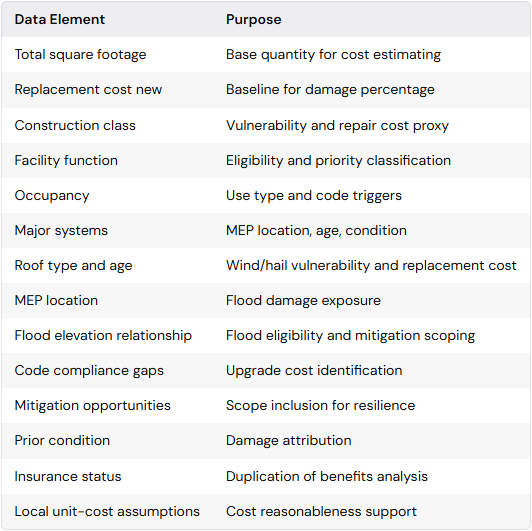

Smart Asset Registry Data Model: The Core Data Fields

A FEMA-ready Smart Asset Registry should be designed as a flat file at the base level — one row per location or one row per asset component, with no merged cells, consistent units, and clean alpha-numeric headers. The following data model serves as comprehensive guidance.

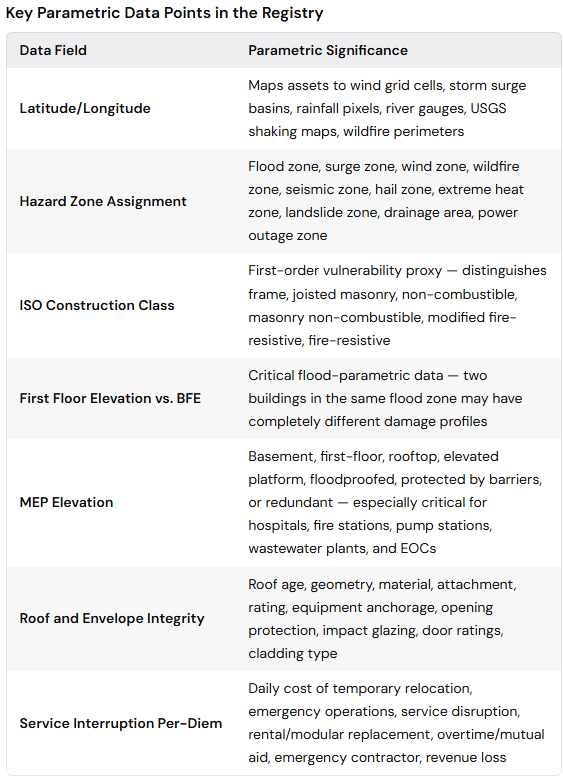

1. Identity and Geospatial Fields

Every asset should include:

Asset ID

Location ID

Facility name

Facility type

Department/agency owner

Legal owner

Operator

Street address

City

State

ZIP code

County

Jurisdiction

Latitude/Longitude

Congressional district

FEMA region

Tribal/non-tribal indicator

Why it matters: Precise geocoding maps assets to hazard grids, wind cells, surge basins, and flood zones. Without coordinates, parametric triggers and damage attribution are unreliable.

2. FEMA Eligibility and Classification Fields

Every asset should include:

Applicant legal responsibility

FEMA PA category (A through G)

Facility type

Critical service flag

Essential governmental service flag

Pre-disaster use description

Ownership documentation link

Insurance schedule link

Pre-disaster condition evidence link

Prior disaster damage record

Why it matters: Current PA eligibility requires the work to be disaster-related, in the designated area, and the legal responsibility of an eligible applicant. The registry should help prove those elements quickly.

3. Value and Cost Fields

Every asset should include:

Building value

Contents/equipment value

Business interruption or service interruption value

Replacement cost new

Replacement cost per square foot

Date of valuation

Escalation index

Local cost adjustment factor

Demolition cost factor

Debris removal factor

Soft cost factor

Design/engineering factor

Permitting factor

Construction contingency

Management cost factor

Why it matters: Proposed §409 estimates must include associated expenses such as labor, management costs, materials, and other costs to repair, restore, reconstruct, or replace the impacted facility.

4. COPE and Engineering Fields

Every asset should include:

ISO construction class

Structural system

Year built

Renovation years

Number of stories

Square footage

Basement flag

Basement area

First floor elevation

Base flood elevation

MEP location (basement, first floor, rooftop, elevated platform, floodproofed)

MEP elevation

Floodproofing status

Roof age

Roof geometry

Roof material

Roof attachment type

Roof rating

Roof equipment anchorage

Opening protection

Impact glazing

Door ratings

Cladding type

Sprinkler status

Sprinkler type

Alarm type

Public protection class

Utility dependencies

Generator capacity

Backup power type

Essential service continuity features

5. Hazard and Mitigation Fields

Every asset should include:

Flood zone (FEMA designated)

Surge zone

Wind zone

Wildfire zone

Seismic zone

Hail zone

Extreme heat zone

Landslide zone

Drainage/watershed area

Power outage zone

Base flood elevation

First floor elevation

MEP elevation relative to BFE

Floodproofing status

Backup power type and capacity

Mitigation opportunities identified

Code upgrade factor

Nature-based protection if applicable

Retrofit status

6. Parametric Trigger Fields

Every asset should include:

Trigger zone assignment

Trigger data source (e.g., wind grid cell, river gauge, rainfall pixel)

Trigger threshold

Vulnerability coefficient or fragility curve assignment by hazard

Payout tier

TIV used for payout calculation

Service interruption per-diem

Business interruption daily cost if applicable

Daily cost of temporary relocation

Daily cost of emergency operations

Daily cost of service disruption

Daily rental/modular replacement cost

Daily overtime/mutual aid cost

Daily emergency contractor cost

Calculation agent

Settlement protocol

Basis risk notes

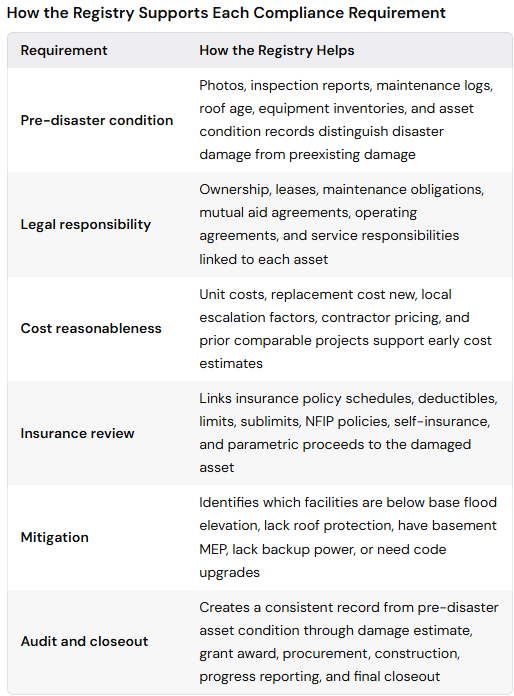

7. Documentation and Evidence Fields

Every asset should include links or references to:

Ownership/lease documents

Insurance policy schedules

NFIP policies

Self-insurance documentation

Pre-disaster condition photos

Inspection reports

Maintenance logs

Roof age records

Equipment inventories

Asset condition records

Drawings and specifications

Prior comparable project cost data

Mutual aid agreements

Operating agreements

Service responsibility records

How the Smart Asset Registry Supports FEMA Upfront Funding

If a future FEMA PA model moves toward upfront funding based on initial estimates, the Smart Asset Registry becomes the applicant's evidence engine.

Pre-Disaster Data: Questions the Registry Answers Before Any Event

What was the facility before the disaster?

Who owned it?

Who had legal responsibility?

What was its use?

What was its pre-disaster condition?

What was its replacement cost?

What construction system was used?

What systems were in the basement?

What systems were elevated?

What codes and standards may be triggered?

What mitigation measures are appropriate?

What insurance applies?

What local cost data should be used?

What prior damage or deferred maintenance existed?

Post-Disaster Data: Questions the Registry Answers Immediately After an Event

What hazard intensity reached the asset?

What components are likely damaged?

What is the estimated percent damage?

What is the initial base cost?

What soft costs apply?

What mitigation costs should be included?

What insurance proceeds or parametric payouts may duplicate or complement the funding?

What scope can be submitted for upfront grant funding?

This is especially important because current PA cost eligibility depends on more than damage. FEMA PA requires eligibility of the applicant, facility, work, and costs. A Smart Asset Registry does not guarantee FEMA eligibility — it makes the eligibility and estimate process faster, cleaner, and more defensible.

The Parametric Trigger Layer: Turning the Registry into a Liquidity Engine

Parametric insurance pays based on an agreed event index, not a traditional loss adjustment. The trigger might be wind speed, flood depth, rainfall total, storm surge height, earthquake shaking, heat index, wildfire footprint, or river gauge height.

The parametric-registry link consists of three components:

Index — A verifiable data point such as wind speed, peak ground acceleration, or gauge height

Threshold — The intensity at which payout activates

Payout Function — The pre-agreed percentage of TIV or other value measure paid when the trigger is met

A traditional SOV can support a crude parametric product because it provides TIV by location. But a Smart Asset Registry supports a better parametric product because it explains how different assets respond to the same hazard.

Example: A Class 1 wood-frame public works garage may suffer severe wind damage at a lower wind speed than a Class 6 fire-resistive building — even if both have the same TIV. The same flood depth that causes 200,000 in damage to a building with elevated MEP may cause \2 million in damage to an identical building with basement MEP.

Settlement Protocol: How the Smart Registry Shortens Time to Cash

A traditional indemnity claim asks: What damage occurred, what does the policy cover, what is excluded, what is the actual repair cost, and what proof supports the claim?

A parametric settlement protocol asks: Did the agreed event occur at the agreed intensity, at the agreed location, according to the agreed data source, and what payout does the schedule require?

Municipal Parametric Settlement Workflow

Step 1 — Event Occurs. A hurricane, flood, earthquake, or wildfire impacts the jurisdiction.

Step 2 — Index Confirmed. An independent data source (e.g., NOAA, USGS, third-party weather station network) confirms wind speeds, flood depths, rainfall totals, or ground shaking intensity at the asset's coordinates.

Step 3 — Registry Cross-Reference. The Smart Asset Registry cross-references the event data against each asset's trigger zone, vulnerability coefficient, and payout assignment.

Step 5 — Settlement Verification. Payout is verified and pre-agreed settlement protocol is executed.

Step 6 — Liquidity Injection. Funds are deployed for emergency work, temporary facilities, debris removal, pumps, generators, shelters, professional estimates, engineering, or non-federal match strategy.

This is where the Smart Asset Registry aligns with FEMA readiness. It does not replace FEMA — it supplies rapid liquidity while FEMA eligibility, cost estimating, environmental review, insurance review, and grant processing proceed in parallel.

Basis Risk: The Central Technical Problem

Parametric insurance has one unavoidable challenge: basis risk — the mismatch between the payout and actual loss. A policy may pay when damage is lower than expected, or fail to pay enough when damage is higher than expected.

The more granular the registry — especially with secondary COPE data — the lower the basis risk. Municipalities may use a parametric-first layer for immediate liquidity followed by a traditional indemnity layer for the tail of the loss.

Five Ways a Smart Asset Registry Reduces Basis Risk

1. Better Geocoding. Precise coordinates prevent the wrong hazard intensity from being assigned to the wrong asset.

2. Better Vulnerability Classification. ISO class, roof type, MEP elevation, opening protection, floodproofing, and retrofit status help differentiate assets rather than treating them uniformly.

3. Better Trigger Zoning. Assets can be grouped into rational zones: coastal surge, inland rainfall, riverine flood, wind grid, wildfire interface, seismic basin, or drainage catchment.

4. Better Payout Curves. Instead of one flat payout for all buildings, payout curves can vary by facility class, construction type, hazard, and criticality.

5. Better Hybrid Design. A public entity can use parametric insurance for immediate liquidity and traditional insurance, FEMA PA, reserves, or bond proceeds for longer-tail reconstruction.

The key is not to make parametric insurance pretend to be indemnity insurance. The key is to design parametric coverage for what it does best: speed, liquidity, transparency, and pre-agreed settlement.

Smart Asset Registry and FEMA Compliance: Avoiding the Wrong Message

The Smart Asset Registry should not be marketed as a way to bypass FEMA rules. It should be marketed as a way to prepare better FEMA submissions.

Current FEMA PA eligibility still requires disaster causation, designated-area location, and legal responsibility (44 CFR § 206.223). FEMA also evaluates facility eligibility, work eligibility, cost reasonableness, insurance, environmental and historic compliance, procurement, and documentation.

A Smart Asset Registry helps with those requirements by organizing evidence before the disaster.

Under proposed §409, annual progress reports would include funded projects, permitted and commenced projects, completed projects, and remaining project status, with reports made publicly available. A Smart Asset Registry can become the backbone of that reporting system.

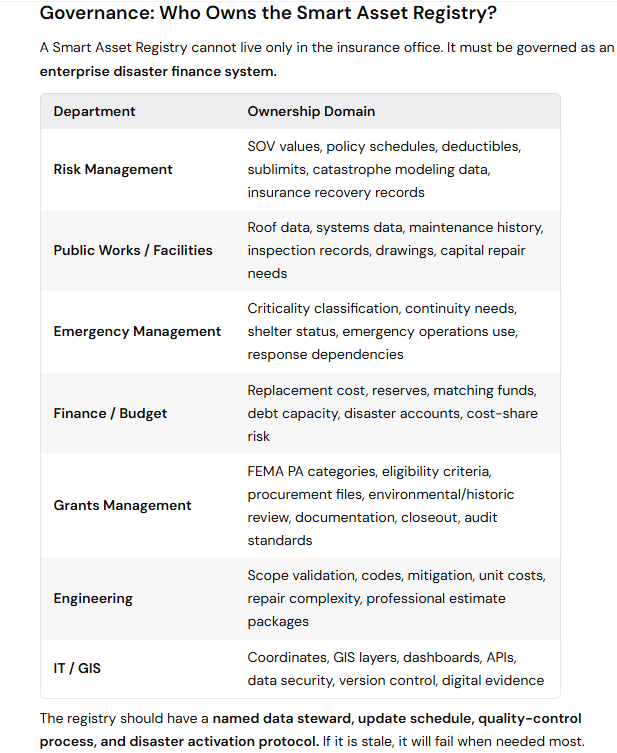

The registry should have a named data steward, update schedule, quality-control process, and disaster activation protocol. If it is stale, it will fail when needed most.

Implementation Roadmap: From SOV to Smart Asset Registry

A practical transition can be staged in seven phases. Each phase builds on the previous one, allowing organizations to start with minimal investment and grow toward full capability.

Phase 1 — Clean the Existing SOV

Start with what exists:

Remove merged cells

Create one row per location

Standardize location IDs

Add latitude/longitude

Validate addresses

Standardize building values

Separate building, contents, equipment, and service interruption values

Add county and jurisdiction fields

Add facility owner and operator

Phase 2 — Add FEMA Eligibility Fields

Applicant legal responsibility

FEMA PA category (A–G)

Facility type

Critical service flag

Essential governmental service flag

Pre-disaster use

Ownership documentation link

Insurance schedule link

Pre-disaster condition evidence link

Phase 3 — Add Engineering and COPE Fields

ISO construction class

Structural system

Year built

Renovation years

Roof age/type/geometry

Number of stories

Basement flag

MEP location

Sprinkler status

Alarm type

Public protection class

Opening protection

Utility dependencies

Phase 4 — Add Hazard and Mitigation Fields

Flood zone

Base flood elevation

First floor elevation

MEP elevation

Wind zone

Seismic zone

Wildfire zone

Floodproofing status

Backup power

Mitigation opportunities

Code upgrade factor

Nature-based protection if applicable

Phase 5 — Add Cost Estimating Fields

Replacement cost new

Unit cost per square foot

Local cost factor

Escalation factor

Demolition factor

Debris factor

Soft cost factor

Management cost factor

Design/engineering factor

Contingency

Damage percentage assumptions

Rapid estimate formula output

Phase 6 — Add Parametric Fields

Trigger zone

Trigger data source

Trigger threshold

Payout tier

Vulnerability curve

Vulnerability coefficient

TIV used for payout

Service interruption per-diem

Calculation agent

Settlement protocol

Basis risk notes

Phase 7 — Build Dashboards

Create dashboards for:

Highest TIV assets

Most critical assets

Highest flood exposure

Basement MEP risk

Roof age risk

Uninsured/underinsured assets

Parametric trigger exposure

FEMA PA estimate readiness

Mitigation priority

Cost-share resilience evidence

The New Disaster Finance Standard

The Statement of Values is not obsolete. It is incomplete.

For insurance placement, the SOV remains the starting point. But for the future of FEMA Public Assistance — upfront funding, cost-estimate-driven recovery, parametric liquidity, and fiscal resilience — applicants need a smarter structure.

A Smart Asset Registry turns the SOV into a recovery operating system.

It connects:

Insurance values

FEMA eligibility

Pre-disaster condition

Engineering data

Hazard exposure

Replacement cost

Mitigation

Parametric triggers

Cash-flow planning

Audit-ready closeout

If HR4669's proposed §409 model or similar FEMA Review Council concepts move forward, the applicants that succeed will be those that can rapidly submit credible initial cost estimates backed by professional data. The proposed §409 text places cost estimates, licensed professionals, mitigation, labor, materials, management costs, review deadlines, funding availability, and annual reporting at the center of the new model.

That makes the Smart Asset Registry one of the most important disaster finance tools a state, local government, tribal government, public authority, school district, utility, transportation agency, or eligible nonprofit can build before the next disaster.

Final Message

The future FEMA PA applicant will not win by having a spreadsheet of insured values.

The future applicant will win by having a verified, geocoded, engineered, cost-ready, insurance-linked, parametric-enabled Smart Asset Registry that can convert damage into defensible funding requests within days — not years.