1. Introduction: The High-Speed Recovery Illusion

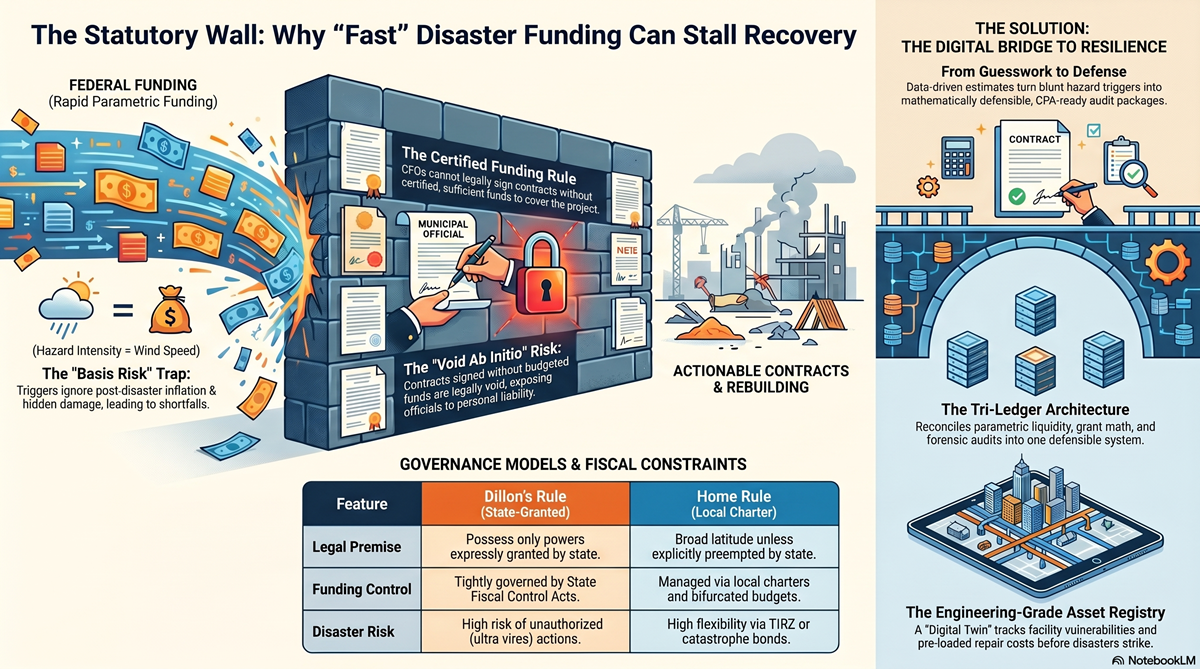

In the immediate aftermath of a disaster, the political and social pressure to secure funding is absolute. To meet this demand, federal policy is undergoing a significant paradigm shift, moving away from slow, itemized reimbursement models toward the "RAPID" funding approach proposed in H.R. 4669. This model promises upfront, formula-driven grants within 30 days, triggered by "parametric" data—such as peak wind speeds or flood depth measurements—rather than granular damage assessments.However, for those responsible for municipal finance, this promise of "immediate liquidity" represents a dangerous statutory trap. As a Chief Policy Strategist, I must warn that the fundamental tension lies in a harsh reality: a macro-level hazard trigger is not a construction cost estimate. When federal speed results in an understated grant, it hits a "statutory wall" of local budget laws, transforming a procedural hurdle into a total mathematical collapse. This creates a legal bottleneck where reconstruction halts because officials cannot legally commit to projects that lack sufficient, certified funding.

2. Takeaway 1: Speed is No Match for the "Statutory Wall"

A foundational pillar of municipal finance is the Certified Funding Rule. This rule prevents governments from entering into binding obligations without the certified fiscal capacity to fulfill them. Consequently, a Chief Financial Officer (CFO) cannot legally execute a construction contract based on an "initial allocation" or a mere promise of federal funds.To satisfy auditors and remain compliant with the Stafford Act and 2 CFR § 200 (Uniform Administrative Requirements) , funding must be categorized correctly and legally bound before any work begins. An "initial allocation" fails to meet the legal threshold of committed funding, which requires an executed and legally bound federal grant agreement."The core tension lies in the fact that a macro-level hazard trigger is not a construction cost estimate. When federal speed results in an understated grant, it hits the 'statutory wall' of local budget laws that prohibit officials from committing to projects without certified, sufficient funds."

3. Takeaway 2: Your City’s "Legal DNA" Dictates Your Flexibility

The authority of a local official to rebuild is governed by the jurisdiction’s specific "legal DNA." Whether your municipality operates under Dillon’s Rule or Home Rule determines the boundaries of your fiscal authority and your exposure to liability.| Feature | Dillon’s Rule (General State Laws) | Home Rule (Charter Framework) || ------ | ------ | ------ || Legal Premise | Municipalities possess only powers expressly granted by the state legislature. | Cities manage local affairs unless explicitly preempted by state law. || Funding Control | Tightly governed by Uniform Municipal Budget Laws and Local Government Fiscal Control Acts . | Managed via local charters; requires a strict bifurcated budget (Operating vs. Capital). || Disaster Financing | Static statutory pathways; alternative risk financing often prohibited without new state acts. | High flexibility; can utilize alternative risk stacks like TIRZ, 4B taxes, or catastrophe bonds. |

Under Dillon’s Rule, there is an existential risk of ultra vires actions. If an official signs a contract for an unbudgeted project, the contract is considered void ab initio (void from the beginning), exposing the official to personal and professional liability. Even under Home Rule, strict "appropriation ordinances" typically require a project to be fully funded before it can move from a Capital Improvement Plan (CIP) to an actionable contract.

4. Takeaway 3: The Danger of "Basis Risk" in Blunt Instruments

In risk finance, "Basis Risk" is the gap between a parametric payout and the actual loss incurred. This gap is the primary catalyst for the failure of rapid recovery models. Parametric triggers, such as wind-speed sensors, are "blunt instruments" that provide data on storm intensity but fail to account for the actual damage to specific infrastructure.A sensor cannot detect facility-specific realities that drive up costs, such as:

- Electrical corrosion in switchgear or the erosion of foundations (scour).

- Demand surge (the post-disaster inflation of labor and material costs).

- Selective demolition and hazardous debris removal.

- Legally mandated building code and ADA upgrades.Relying on these blunt triggers ignores the actual pricing of reconstruction, leading to grants that are mathematically insufficient to cover the work required.

5. Takeaway 4: The Failure Chain of Understated Grants

When the RAPID model’s macro-hazard data results in an insufficient grant, it initiates a four-step failure chain that can stall recovery for years:

- The Understated Grant: Basis Risk—the gap between hazard data and engineering reality—results in a funding offer that ignores demand surge and hidden variables like selective demolition.

- The Local Shortfall: By accepting a fixed grant under these models, the local government waives traditional cost-reimbursement protections. This leaves taxpayers responsible for 100% of any overrun risk.

- The Legal Wall: Because the budget is out of balance, the City Council cannot legally appropriate the missing millions, and the CFO is statutorily barred from certifying the contract.

- Stalled Infrastructure: Reconstruction stops. The community remains in ruin because the "speedy" funding was mathematically insufficient to trigger a legal contract.

6. Takeaway 5: The "Digital Twin" as a Legal Shield

To bridge the gap between legal risk and engineering reality, municipalities must adopt an Engineering-Grade Asset Registry . This "Digital Twin" acts as a technical bridge, allowing officials to intersect hazard data with component-level vulnerabilities before a shortfall occurs, providing a defensible fiscal shield.A defensible recovery registry must be able to answer these five questions:

- Question 1: What was exposed? (Requires geospatial footprints and facility hierarchy).

- Question 2: How intense was the hazard? (Intersection with high-water marks, wind swaths, or ShakeMaps).

- Question 3: Which components are vulnerable? (Component-level data, such as location of MEP systems or roof age).

- Question 4: What is the repair cost? (Using pre-loaded unit costs and "damage-to-cost" formulas).

- Question 5: What portion is insured? (Integration with insurance policy schedules and deductibles).

7. The Future of Resiliency: The Tri-Ledger Architecture

To satisfy the stringent requirements of auditors and CFOs, disaster data should be managed through a "Tri-Ledger Architecture." This system provides immutable evidence for recovery across three layers:

- Parametric/Liquidity Ledger: Confirms the event threshold and releases initial cash flow.

- Capital/Grant Ledger: Converts hazard intensity into a mathematically defensible, facility-specific cost estimate using the asset registry.

- Forensic/Insurance Ledger: Validates spending and prevents Duplication of Benefits (DOB) .This architecture produces "CPA-ready audit packages," which are essential for defending the municipality against federal clawbacks and satisfying the transparency requirements of 2 CFR § 200.

8. Conclusion: Accuracy Over Speed

The core takeaway for municipal leaders is that a disaster trigger is not a cost estimate. Releasing funds based on hazard data without engineering data inevitably transfers the entirety of the financial risk to the local level.The law does not grant exceptions for "disaster urgency" or "good intentions." Without certified, appropriated funds that meet the requirements of Local Government Fiscal Control Acts, officials are legally powerless to sign contracts. Embracing the "Digital Imperative" through a pre-disaster Asset Registry is the only way to reconcile the need for speed with the accuracy required by law.As a leader, is your municipality equipped with a "Digital Twin" capable of turning immediate liquidity into a legally defensible rebuilding plan?